AI for Mid-Market Insurance: What Actually Works

Claims intake, submission triage, and status updates deliver real ROI for $50M-$80M insurers today. Fraud models and full automation are still vendor promises.

Most insurance AI content is written for carriers with $1B+ in premiums and dedicated innovation teams. If you run a $50M regional insurer, MGA, or TPA, the playbook is different. Claims intake automation, underwriting submission triage, and customer status updates deliver real ROI today. Predictive underwriting, fraud detection models, and full process automation are still vendor promises for companies your size. Start with the workflow that costs you the most hours per week, not the one with the flashiest demo.

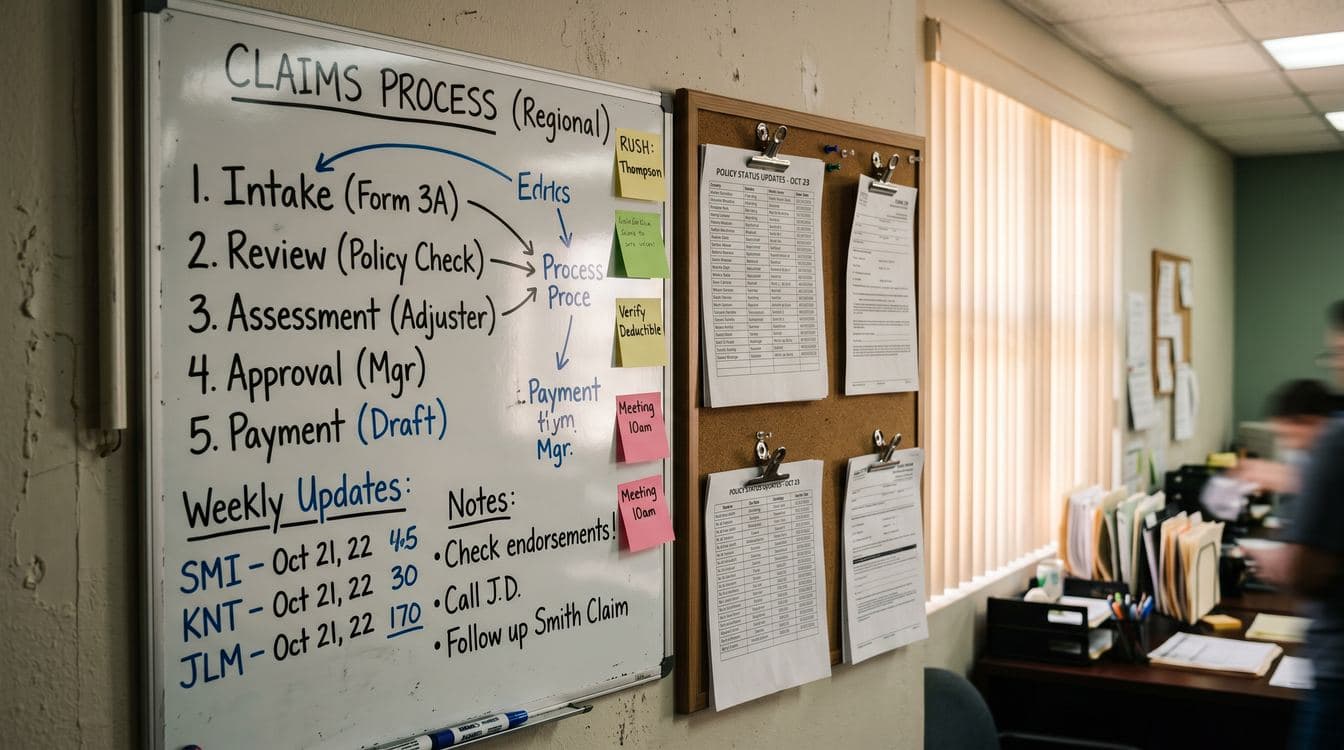

Your operations team is spending hours every week on work that should take minutes. A new claim comes in by email, a CSR reads it, copies data into the system, assigns an adjuster, and sends a confirmation. The same pattern repeats for broker submissions: someone opens the email, pulls out the ACORD form, checks the lines of business, and routes it to the right underwriter. Then policyholders call on Monday morning asking for a status update that nobody prepped Friday.

None of this requires human judgment. All of it is consuming human hours.

The gap between what AI can do for insurance and what actually gets deployed at mid-market shops is significant. BCG found that only 7% of companies across industries have scaled AI beyond pilots. WTW research points to a 35-percentage-point adoption gap between large carriers and mid-market operators. That gap is not because the technology does not work. It is because most vendors sell to the enterprise, and the use cases they demo first (real-time fraud scoring, full underwriting automation, predictive loss models) require data infrastructure and IT capacity that a $60M company simply does not have.

Here is what does work, and what does not, when you are running operations at that scale.

The Three Workflows Worth Automating Now

Claims Intake and FNOL Triage

First Notice of Loss is one of the most document-intensive, time-sensitive parts of claims. An AI intake system reads the FNOL email or form, extracts the key fields (claimant, date of loss, policy number, loss type, contact information), scores severity based on loss type and coverage limits, and routes to the right adjuster queue.

At a 20-person firm processing 200 claims per month, moving FNOL handling from 15+ minutes of manual work to under 60 seconds changes your unit economics. That is roughly 60 hours per month returned to staff who should be making coverage decisions, not copying fields.

The key integration point is your Agency Management System. If you are on Applied Epic or Vertafore, this is a solved problem. FNOL automation tools built on top of these platforms can be deployed in under six weeks. You do not need a new core system. You do not need a data science team. You need an AI that reads email and PDFs and writes to the right fields.

The realistic ROI range for shops this size is 3x to 5x, factoring in labor time recovered, reduced error rates, and faster adjuster assignment. Those numbers come from implementation data, not vendor projections.

Underwriting Submission Triage

Underwriters at mid-market carriers and MGAs spend roughly 40% of their time on administrative work, according to Accenture research. The biggest chunk of that is processing inbound broker submissions: opening emails, pulling attachments (ACORD 125s, SOVs, loss run reports), deciding whether the risk fits appetite, and routing accordingly.

AI triage for submissions extracts structured data from those documents with 90%+ accuracy out of the box. More importantly, it can apply your appetite rules before a human ever opens the email. Does this risk fall within your geographic footprint? Is the SIC code one you write? Is the requested coverage limit within your authority? If three of those checks fail, the submission gets declined automatically with a templated response. If it passes, it lands in the underwriter's queue with all the relevant data already extracted.

Tools like SortSpoke and Indico are built specifically for this. They are not generic document processors that happen to work on insurance forms. They are trained on ACORD forms, loss runs, and broker submissions. They connect to Guidewire, Duck Creek, Salesforce, and most AMS platforms without custom development work.

The benchmark numbers from companies that have deployed these tools: 5x faster submission processing, 50% reduction in turnaround time, and 70% less manual work for the underwriting team. Those are achievable at your scale. The setup timeline is four to eight weeks, not a multi-year implementation.

This is also a growth story, not just a cost story. If you can process submissions in hours instead of days, your brokers notice. Faster time-to-quote is a competitive advantage in commercial lines.

Customer and Policy Status Updates

The phone calls your CSRs handle most often are not complex. "Where is my claim?" "Is my renewal being processed?" "Did you receive my documents?" These questions require your staff to log in to a system, look up the record, and read back information that already exists.

An AI agent can handle this. It reads from your AMS or claims system, interprets the current status, and responds via SMS, email, or web chat with an accurate, personalized update. No hallucination risk because the agent is reading live system data, not generating from training data. No compliance exposure because the response is templated around the actual record.

The ROI calculation is straightforward: count how many status-update calls and emails your CSR team handles per week, multiply by average handle time, and that is your labor cost. Even recovering 30% of that time is meaningful when you are running a lean team.

The integration work is real but not novel. If your AMS has an API (most modern ones do), this is a two-to-four week build.

What Does Not Work Yet at Your Scale

Deloitte found that 76% of insurers have deployed generative AI in some form. Most of what they deployed is not what the vendor pitch decks led with in 2023.

The following use cases are either genuinely not ready for mid-market operators or require infrastructure you do not have:

Predictive underwriting models. Building a model that predicts loss ratios on new risks requires years of your own claims and exposure data, clean and in a warehouse. Most $50M-$80M carriers do not have a data warehouse. Most do not have clean historical data going back far enough to train on. The vendors who promise this often need 18 to 24 months of data prep before the model is useful.

Real-time fraud detection. The tier-one carriers doing this well have hundreds of thousands of claims per year to train on, dedicated ML teams, and integration with external data providers like LexisNexis and Verisk. At your volume, the false-positive rate of a fraud model will create more manual review work than it eliminates.

End-to-end claims automation. Full straight-through processing on complex claims is a carrier-scale problem. For a TPA or regional carrier, the edge cases will swallow you. AI-assisted triage and intake is the right first step. Full automation is a three-to-five year roadmap, not a six-month project.

Customer-facing chatbots for complex inquiries. Status updates work. Coverage questions, billing disputes, and claims appeals do not. If a policyholder asks something outside the narrow lane you have trained for, the chatbot either hallucinates or routes to a human. You have added complexity without removing the human. Scope chatbot automation narrowly or do not do it.

How to Choose Where to Start

The decision is not which AI use case has the best demo. It is which workflow is costing you the most hours per week right now.

Pull your team's time logs for the last month. If you do not have formal time tracking, spend one week having each person note where their time goes in 30-minute blocks. You will see a pattern. The workflows that account for the most hours with the least decision-making are your automation targets.

A simple scoring framework:

- Hours per week consumed (higher = higher priority)

- Human judgment required (less judgment = easier to automate)

- Data already in structured form (more structured = shorter implementation)

- Integration complexity (does your AMS have an API? Does it connect to the tools you are evaluating?)

FNOL intake typically scores highest on all four dimensions. Submission triage is close behind. Status updates are the fastest to implement because the data already exists and the response scripts are narrow.

See also the AI vendor evaluation guide for operators without a CTO if you are still working through how to assess the tools before buying. And if you are deciding whether to build custom or buy off-the-shelf for any of these workflows, the build vs. buy guide for mid-market operators covers the tradeoffs in detail.

The Budget and Timeline Reality

For a company your size, the workflows above do not require enterprise software budgets.

FNOL automation for a 20-person shop: $15,000-$25,000 to build and integrate, plus ongoing API and maintenance costs. Payback period under six months at 60 hours per month recovered.

Submission triage for an MGA processing 300 submissions per month: SaaS tools in this category run $2,000-$5,000 per month. At 5x faster processing and one underwriter's recovered time, the math works in under two months.

Status update automation: $8,000-$15,000 one-time build cost if you go custom, or $500-$1,500 per month for a SaaS solution with AMS connectors. Most recoveries happen in the first 30 days.

None of this requires hiring an AI team. It requires finding the right implementation partner and being clear about which workflow you are solving first.

Start Narrow, Prove It, Then Expand

The mid-market insurance operators who are making real progress with AI in 2026 did not start with a transformation roadmap. They started with one workflow, measured what changed, and then decided whether to expand.

Pick the workflow your team complains about most. Not the one with the best vendor demo. Not the one that sounds most innovative. The one that is grinding your people down and producing predictable, repeatable output that does not require judgment.

That is where AI delivers. The rest comes later.

If you want a second opinion on whether a specific workflow is worth tackling at your size, Granular publishes short takes on these decisions every week. Subscribe below to get them when they come out, or forward this to someone on your team who is carrying the inbox load.

Keep Reading

- How to Cut Claims Processing Time Without Replacing Your Core System — A step-by-step playbook for speeding up claims operations by automating around your existing AMS, not ripping it out.

- How to Evaluate AI Vendors Without a CTO — A practical framework for operators who need to assess AI tools and implementation partners on their own.