How $50M Asset-Based Lenders Cut Borrowing Base Cycle to 1 Day

Mid-market ABL collateral analysts spend 3 to 5 days reconciling each Borrowing Base Certificate. Here is the workflow that compresses it to under a day.

TL;DR. Senior collateral analysts at mid-market ABL firms spend 3 to 5 days per Borrowing Base Certificate, most of it ingesting heterogeneous AR aging files, applying ineligibility rules borrower by borrower, and reconciling dilution. LoanWatch's analyst time study clocks 4 hours per clean BBC and 48 hours per month per analyst before exceptions. Seven workflow moves that sit on top of any core platform (Solifi, Lendscape, FIS Asset Finance) compress the cycle to under a day and double analyst portfolio capacity at the same fully loaded comp.

If you are running operations at a $50M asset-based lender, you know the math. Senior collateral analyst at $130K to $150K fully loaded. Ten to fifteen active borrowers. Three to five days per Borrowing Base Certificate when the AR aging arrives in a format nobody saw coming. By the time you reconcile the cross-aging, apply the concentration cap, run the dilution waterfall and check it against last month, half the week is gone. Then the next BBC lands.

The fix is not a vendor's "AI for ABL" pitch. It is the same move you would run on a manufacturing line: figure out where the hours go, attack the worst step. Most $50M ABL shops can cut BBC cycle time from 3 to 5 days to under 24 hours without replacing their core platform.

What a Borrowing Base Certificate Actually Requires

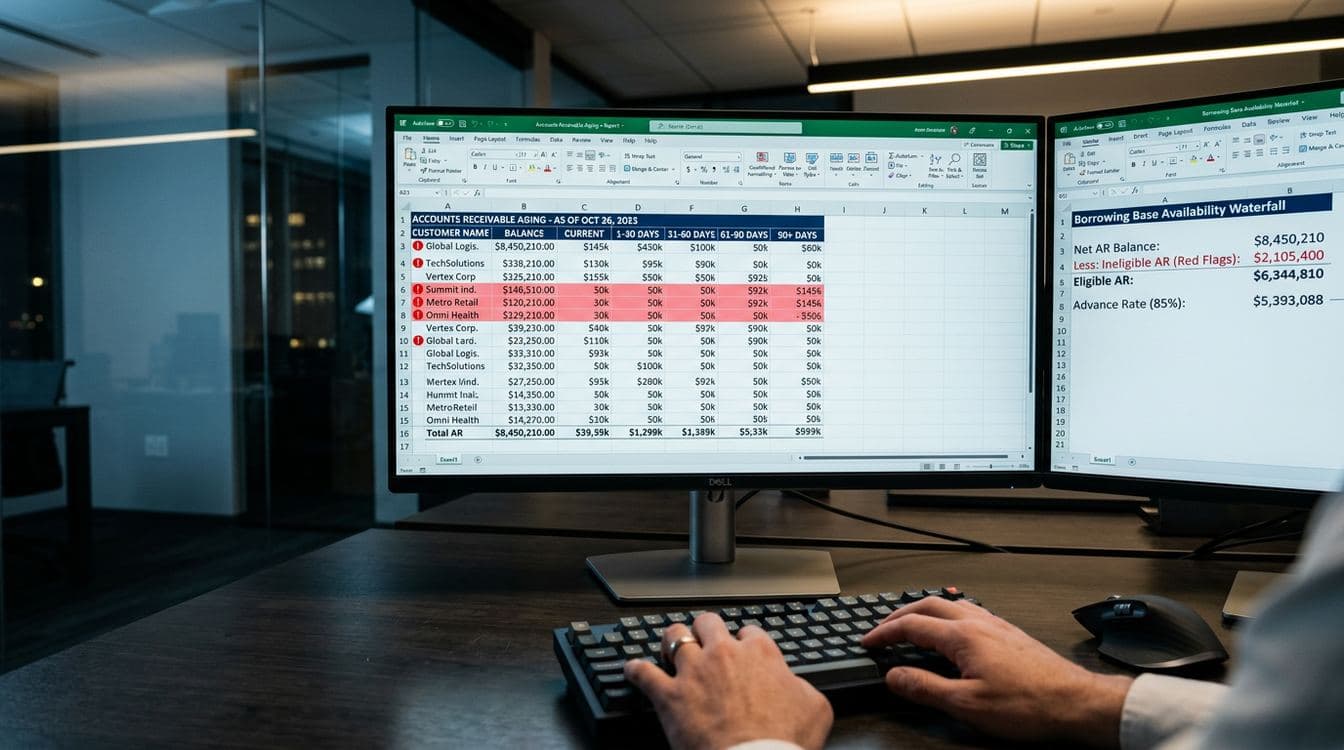

Pull the OCC Comptroller's Handbook on Asset-Based Lending and the standard BBC waterfall has not moved since 1995. Gross trade AR. Subtract ineligibles (over 90 days, contra accounts, foreign, government, intercompany, disputed). Apply the concentration cap (typically 10 to 20 percent of the borrowing base per customer, with a 10 percent trigger threshold). Multiply by the advance rate (70 to 85 percent for AR, up to 90 percent on B2B trade receivables). Add eligible inventory at its advance rate (typically 50 percent). Net out reserves: dilution, ineligible cap, fee, environmental, anything custom in the loan agreement. Output: Availability.

Eight line items. Don Clarke, the SFNet Hall of Fame trainer who has run ABL training at GE Capital, JPMorgan, Lloyds and Barclays, walks the line-by-line waterfall in detail. His benchmark: a clean BBC should be auditable in under 15 minutes per certificate. The reality at most mid-market shops is 3 to 5 days.

The math on why is not subtle.

Where the 5 Days Actually Go

LoanWatch ran a time study on regional bank ABL analysts and got a clean decomposition: roughly 4 hours per BBC before exception handling, 48 hours per month per analyst, 12 BBCs per analyst. Their breakdown of those four hours:

- 20 to 30 minutes ingesting the AR aging from PDF, Excel, or the borrower's accounting system into the analyst's BBC template

- 45 to 60 minutes applying eligibility rules (the over 90, contra, foreign, disputed, intercompany sweep)

- 35 to 45 minutes reconciling this month's BBC against last month's (the cross-aging check that catches stale receivables masquerading as fresh ones)

- 15 to 20 minutes assembling the documentation packet for the credit file

That is the clean case. Now the realistic case. The borrower's controller added a new tab to the Excel file because they switched ERPs. The "Customer Name" column has 47 spelling variants for the same customer. A $1.8M receivable from a parent company is split across three subsidiary names that need cross-aging for concentration. The borrower changed their cutoff date. Three customers crossed the 10 percent concentration threshold this month.

A clean BBC takes 4 hours. A messy one takes 2 to 3 days. Averaged across a 12-borrower portfolio: 3 to 5 days per cycle, every cycle.

Don Clarke's analysis of dilution reserve mechanics shows reserves alone can compress availability by 10 to 25 percent of the borrowing base. That is the borrower's number, and the analyst's too: every basis point of dilution the analyst miscalculates becomes a CFO complaint or a covenant problem six months later.

The Seven-Step Playbook

These are the seven moves that compress BBC cycle time at a mid-market ABL firm. None of them require ripping out Solifi, Lendscape, or FIS Asset Finance. They sit on top of whatever core platform you already use.

Step 1: Standardize the AR Aging Intake

The biggest time sink is the 20 to 30 minutes reconciling a different file format from each borrower. The fix is not "force every borrower to use your template." Borrowers will not migrate their accounting systems for you. The fix is parser logic on the lender side that handles the four or five formats your portfolio actually submits: QuickBooks-exported Excel, NetSuite-exported CSV, Sage 50 and Sage 100 reports, and the occasional PDF dump from a regional ERP.

The newer ABL platforms have this built in. AIO Logic's AXIS markets direct API connections to QuickBooks and NetSuite, eliminating manual ingestion for borrowers on either system. Where API access is not feasible, parser tooling for the heterogeneous formats your portfolio submits gets 80 percent of the way there.

Time saved: 25 minutes per BBC. Across a 12-borrower portfolio, that is 5 hours per month.

Step 2: Codify the Ineligibility Rules per Borrower

Every loan agreement has its own ineligibility schedule. The over 90 rule is universal. The borrower-specific ones (contra accounts with named related parties, disputed receivables flagged in the borrower's CRM, government receivables capped at X percent) are where mistakes happen. The fix: one ineligibility ruleset per borrower, codified in a structured format your platform or your spreadsheet can apply programmatically.

This is not AI work. It is "open the loan agreement once, encode the rules, never reread them." Almost no mid-market ABL shop does this consistently because the analyst rotates through the portfolio month by month and re-derives the rules from memory or from a wiki entry the analyst who left two years ago last updated.

Time saved: 30 minutes per BBC.

Step 3: Pre-Compute the Cross-Aging Variance

The 35 to 45 minute month-over-month reconciliation is where stale receivables get caught. The mechanic is comparing this month's aging buckets to last month's, customer by customer, looking for receivables that should have aged out (paid) but did not (still on the books, now with a different invoice number).

Your platform already has last month's aging. Run the variance computation programmatically. Surface only the customers with material movement: greater than $50K change, greater than 30-day age shift, or new accounts crossing 1 percent of the borrowing base. The analyst reviews exceptions, not every line.

Time saved: 30 minutes per BBC.

Step 4: Automate the Concentration Cap

The 10 to 20 percent concentration cap on any single customer is a known calculation. The complexity comes from cross-aged parent-subsidiary relationships and from customers that cross the threshold for the first time this month. Both are programmatic. Maintain a customer hierarchy table per borrower (one-time setup, periodic update), then apply the cap programmatically against the eligible AR.

Don Clarke's worked example shows the dilution calculation precisely: Reserve equals (Dilution percent minus Threshold) divided by (1 minus Dilution percent). Moving dilution from 7.5 percent to 6 percent lifts availability roughly $258K per month on a $16M AR pool. Get the calculation right, get it right consistently, and the borrower stops calling about availability.

Time saved: 20 minutes per BBC.

Step 5: Daily Recalculation, Not Monthly

Once Steps 1 through 4 are in place, the bottleneck disappears. You can recalculate availability daily. StarterStack reports clients moving from monthly to daily BBC recalculations across a $200M portfolio, with calculation errors dropping roughly 85 percent and 3x deal capacity without adding analyst headcount.

Your largest borrowers track availability daily anyway. They call the analyst when they want a real-time number. With daily recalculation, the number is already in the portal. The borrower's CFO checks it, makes the draw, moves on. The relationship gets stronger because the lender is faster.

Step 6: Exception-Driven Analyst Review

The analyst's job shifts from running the BBC to reviewing the exceptions: the three customers that crossed concentration thresholds, the cross-aged receivable that grew $400K month over month, the new ineligible bucket the borrower disclosed. Everything else is automatic. At 12 BBCs per month per analyst, you reclaim 3 hours per BBC (36 hours per month) and reinvest them in exception review, which is the high-value work.

Step 7: Field Exam Prep on Demand

The first ABL field exam takes 3 to 5 days on site. The auditor reviews the three most recent BBCs and ties each line back to AR aging, perpetual inventory, and ineligibility calculations. If your workflow is structured and auditable from Step 1, exam prep collapses from a panic project to a one-day file export.

This is the durable competitive advantage. The non-bank ABL lenders that win in 2026 (Siena Lending Group, MidCap Financial, North Mill Capital, Encina Business Credit) are the ones whose analyst desk runs a clean borrower portfolio at 2x the volume per FTE.

What Changes for Your Portfolio

Three things change when BBC cycle time drops from 3 to 5 days to under 24 hours.

First, analyst capacity expands. A senior collateral analyst on a $130K to $150K fully loaded comp basis goes from carrying 10 to 15 borrowers to carrying 20 to 25 without quality loss. At a $50M ABL firm with three senior analysts, that is the difference between a $200M portfolio and a $400M portfolio without adding heads. McKinsey via CEO Weekly puts the cost base reduction at 15 to 20 percent for ABL platforms that automate the post-origination workflow, and post-origination is roughly 90 percent of the operational life of a facility.

Second, borrower relationships improve. The borrowers calling your analyst at 4pm on a Friday asking for availability are doing real treasury work. When the number is already in the portal and accurate, those calls become draw requests instead of complaints. The non-bank ABL market grew 17.5 percent year over year through Q3 2025 per the Secured Finance Network. The lenders pulling away are the ones running faster.

Third, dilution math gets sharper. Daily recalculation means dilution trends surface in real time, not three weeks after the receivable went stale. The analyst catches deterioration before it becomes an availability fight at the next quarterly review.

The non-bank ABL space is mid-cycle in its biggest capital-markets year on record. SFNet's 2025 full-year ABL Survey shows non-bank ABL outstandings up 12.6 percent in Q4 alone. Siena Lending Group closed over $1B in facilities in 2025, with deal sizes from $20M to $350M. The shops scaling fastest are the ones whose BBC workflow can keep up.

FAQ

What is a realistic BBC cycle time for a clean borrower at a $50M ABL firm? A well-run BBC on a structured portfolio borrower (clean ineligibility rules, no concentration issues, daily-recalculation infrastructure in place) should clear in 2 to 3 hours of analyst time. Don Clarke benchmarks the line-item audit at under 15 minutes. Most $50M ABL shops sit at 3 to 5 days because the analyst is reconstructing the workflow each cycle, not because the workflow itself is slow.

Do we need to replace Solifi, Lendscape, or FIS Asset Finance to do this? No. The seven-step playbook sits on top of any of those core platforms. Platforms with native AR aging API connections (AIO Logic AXIS, parts of Solifi) skip Step 1 entirely. Older platforms need a parser layer on the side. Either way, you are not replacing the platform.

How does daily recalculation affect our field exam relationship with the OCC or our state regulator? It improves it. Auditors prefer structured, auditable, repeatable workflows over month-end heroics. The first ABL field exam after you implement daily recalculation is typically the cleanest your firm has run, because the documentation packet is generated continuously, not assembled in a panic the night before.

What is the revenue difference between bank ABL and non-bank ABL operations? Banks generate roughly 3.0 percent revenue as a percentage of outstandings. Non-bank ABL lenders generate 10.7 percent per the SFNet 2025 ABL Survey. The economics support more operational investment per facility, and the shops putting that investment into workflow automation pull away.

The seven-step playbook is the same one we run when we build BBC workflows for mid-market ABL lenders. The analyst desk that was carrying 12 borrowers carries 22. The dilution math gets right. The borrower CFO stops calling. The next facility closes faster because operations can absorb it. If this sounds like your Tuesday morning at the analyst desk, book 30 minutes with us and we will walk you through what a 4-week BBC workflow build looks like.

Keep Reading

- How $50M Equipment Finance Firms Cut End-of-Term Cycles: The same workflow-tightening logic applied to end-of-term contract processing at mid-market equipment lessors.

- Concentration Risk: The Spreadsheet Every Factor Maintains: Why every factoring company runs a shadow concentration spreadsheet, and what changes when you stop.